When it comes to the Canadian banking sector, the last couple of years have been unusual, to say the least. In this blog post, we’ll delve into the current outlook for Canadian banks, explore the challenges they face, and discuss strategies for investors looking to navigate these uncertain waters. The following are my takeaways from a conversation with Gabriel Dechaine, Managing Director Canadian Banks and Insurance Analyst from National Bank Financial

The Unusual Underperformance

One standout trend in the Canadian banking sector is the underperformance of banks in comparison to the broader market. Notably, this has been ongoing for two consecutive years, a rarity in itself. As for three years in a row? That’s uncharted territory as far as we know.

So, why are Canadian banks facing such headwinds? Gabriel Dechaine offers some insights into the challenges ahead:

- Stringent Regulatory Restrictions: The banks are grappling with increasingly stringent regulatory restrictions and capital requirements. While their current capital levels are robust, these requirements continue to rise.

- Expense Inflation: Operating costs are on the rise, putting pressure on profitability.

- Competitive Deposit Rates: Reduced net margins on loans are a concern as deposit rates become more competitive.

- Stagnant Margins: Although higher interest rates typically lead to improved margins, that’s not the current trend.

- Sluggish Mortgage Growth: The growth of mortgages has been slowing down, impacting lending income.

- Rising Impaired Loans: Impaired loan balances are on the rise, which could affect the banks’ bottom line.

- Mortgage Payment Shock: A substantial portion of mortgages at many banks has lengthy amortization periods, potentially leading to payment shocks. These challenges are collectively putting downward pressure on bank earnings.

Dividend Dilemma

For income-oriented investors, dividends are a crucial consideration. The good news is that payout ratios remain elevated but sustainable. However, don’t expect robust dividend growth in the near future.

Furthermore, banks are taking measures to bolster their capital positions, which has led to discounts on their Dividend Reinvestment Plans (DRIPs). Share buybacks are not currently a priority for most banks.

Valuation and Yield

Given these factors, Canadian banks are currently trading below-average valuations, with a price-to-earnings ratio of approximately 9.5, compared to the 10-year average of 10.5. Consequently, the average dividend yield on these banks stands at over 5.25%.

The question on every investor’s mind is whether this is a good time to buy. The answer, of course, depends on various factors. Short-term volatility may persist, potentially driving prices lower. Still, for long-term investors willing to weather the storms, this could be an attractive entry point.

Investment Strategies

Now, let’s discuss some strategies for navigating the Canadian banking landscape:

- Long-Term Entry: Timing the market can be challenging. Consider this a long-term entry point and collect yield while waiting for better times.

- Cost-Efficient Exposure: Most investors already have or should have exposure to Canadian banks. Look for low-cost solutions to maintain your exposure efficiently.

- Explore ETFs: Consider these solutions for switches in your current exposures or as additions. Some ETF options include:

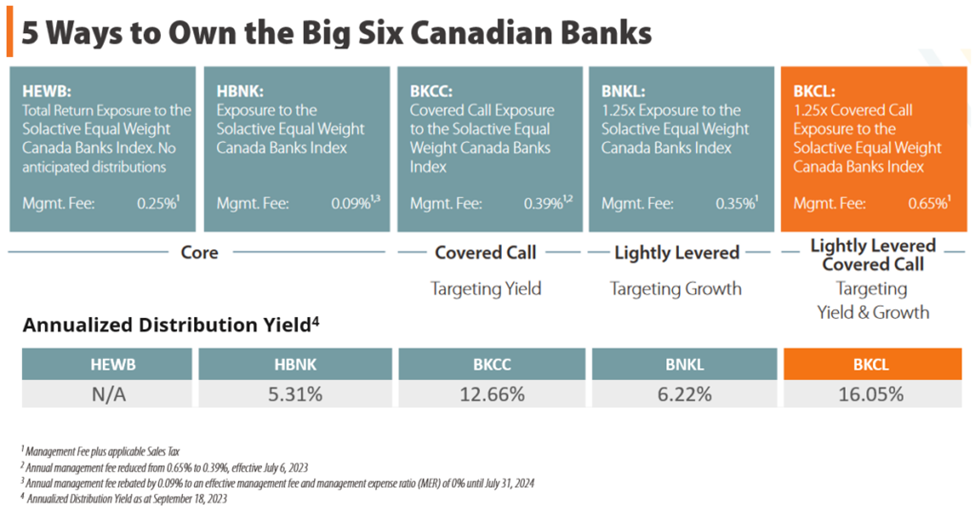

- Global X Equal Weight Banks Index ETF (HBNK) (formerly, Horizons Equal Weight Banks Index ETF): Offering the lowest cost exposure for Canadian banks, with an annualized distribution yield of 5.31%⁴.

- Global X Equal Weight Canada Banks Corporate Class ETF (HEWB) (formerly Horizons Equal Weight Canada Banks Index ETF): A part of the Total Return Corporate Class, suitable for those not needing income, offering tax-efficient growth.

- Global X Equal Weight Canadian Bank Covered Call ETF (BKCC) (formerly Horizons Equal Weight Canadian Bank Covered Call ETF): For more income, consider monetizing volatility by writing covered calls, yielding a tax-efficient ~12%.

- Global X Enhanced Equal Weight Banks Index ETF (BNKL) (formerly Horizons Enhanced Equal Weight Banks Index ETF): Enhanced exposure for bullish investors, offering a higher dividend yield of 6.22%⁴.

- Global X Enhanced Equal Weight Canadian Banks Covered Call ETF (BKCL) (formerly Horizons Enhanced Equal Weight Canadian Banks Covered Call ETF): For those seeking growth and income, it offers a current annualized distribution yield of 16%.

Expert Insights

Gabriel Dechaine’s favourite among Canadian banks right now is RBC, and he highlights that while banks are correlated over time, interim moves can differentiate them. The equal weight exposure strategy, which rebalances twice a year, can help add value by “selling the winners and buying the laggards,” potentially leading to better returns.

Looking Ahead

With deposits continuing to grow, there’s reason to be optimistic about the stock market’s prospects in the coming years. As interest rates start to come down, moving cash back into the markets could present an opportunity in the long term. However, it’s essential to keep in mind that Gabriel’s analysis is focused on the next 6-12 months. In conclusion, the Canadian banking sector faces challenges, but it also offers opportunities for astute investors. Consider your investment horizon, risk tolerance, and the strategies outlined here when navigating the dynamic landscape of Canadian banks.

Jeff Lucyk

Executive Vice-President, Head of Sales, Global X Investments Canada Inc.

Jeff Lucyk is Executive Vice-President, Head of Sales for Global X Investments Canada Inc. Mr. Lucyk is responsible for managing and leading the sales team to identify new business opportunities and enhancing the growth of the firm. He was formerly the Vice-President and National Sales Manager at Norrep Investments. Mr. Lucyk graduated from Brock University with an Honours Degree in Business Administration and holds the Chartered Alternative Investment Analyst (CAIA) designation.

DISCLAIMERS

Commissions, management fees, and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain Global X Funds may have exposure to leveraged investment techniques that magnify gains and losses which may result in greater volatility in value and could be subject to aggressive investment risk and price volatility risk. Such risks are described in the prospectus. The prospectus contains important detailed information about the Global X Funds. Please read the relevant prospectus before investing.

Global X Total Return Index ETFs (“Global X TRI ETFs”) are generally index-tracking ETFs that use an innovative investment structure known as a Total Return Swap to deliver index returns in a low-cost and tax-efficient manner. Unlike a physical replication ETF that typically purchases the securities found in the relevant index in the same proportions as the index, most Global X TRI ETFs use a synthetic structure that never buys the securities of an index directly. Instead, the ETF receives the total return of the index by entering into a Total Return Swap agreement with one or more counterparties, typically large financial institutions, which will provide the ETF with the total return of the index in exchange for the interest earned on the cash held by the ETF. Any distributions which are paid by the index constituents are reflected automatically in the net asset value (NAV) of the ETF. As a result, the Global X TRI ETF receives the total return of the index (before fees), which is reflected in the ETF’s share price, and investors are not expected to receive any taxable distributions. Yields from the underlying holdings and/or index returns are included in the total return of the ETF. This ETF is not expected to make taxable distributions.

Effective June 24, 2022, the investment objectives of the Global X Equal Weight Canadian Bank Covered Call ETF (“BKCC”) (formerly Horizons Equal Weight Canadian Bank Covered Call ETF), were changed following receipt of the required unitholder and regulatory approvals, to seek to provide exposure to the performance of an index of equal-weighted equity securities of diversified Canadian banks (currently, the Solactive Equal Weight Canada Banks Index) and to employ a dynamic covered call option writing program. Previously, the ETF sought exposure to an underlying equal-weight equity portfolio and generally wrote covered call options on 100% of portfolio securities. For more information, please refer to the disclosure documents of the ETFs on www.GlobalX.ca.

BKCL and BNKL (the “Alternative ETFs”) are alternative investment funds within the meaning of the National Instrument 81-102 Investment Funds (“NI 81-102”) and are permitted to use strategies generally prohibited by conventional mutual funds, such as the ability to invest more than 10% of their net asset value in securities of a single issuer, the ability to borrow cash, to short sell beyond the limits prescribed for conventional mutual funds and to employ leverage of up to 300% of net asset value. While these strategies will only be used in accordance with the investment objectives and strategies of the Alternative ETFs, during certain market conditions they may accelerate the risk that an investment in ETF Shares of such Alternative ETF decreases in value. The Alternative ETFs will comply with all requirements of NI 81-102, as such requirements may be modified by exemptive relief obtained on behalf of the ETF.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

The views/opinions expressed herein are solely those of the author(s) and may not necessarily be the views of Global X Investments Canada Inc. All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

Published September 25, 2023

Categories: Articles, Insights

Topics: Canadian Banks